|

Here's the 3 must have traits to be a successful investor - confidence, discipline & patience. This applies to just about everything that's good and worthwhile in life. Check it out.

Annual Asset Class returns are provided by the the Novel Investor - novelinvestor.com/asset-class-returns/

Source: novelinvestor.com Source: novelinvestor.com

Knowing when to be more direct and straightforward is a balance in all relationships-new or old. It is not my style to be conversationally direct unless provoked or I’m angry. As I raise my teenagers, however, I’m direct when needed, but I’m also known to provide all the context clues and allow them the lee-way to figure out certain experiences on their own.

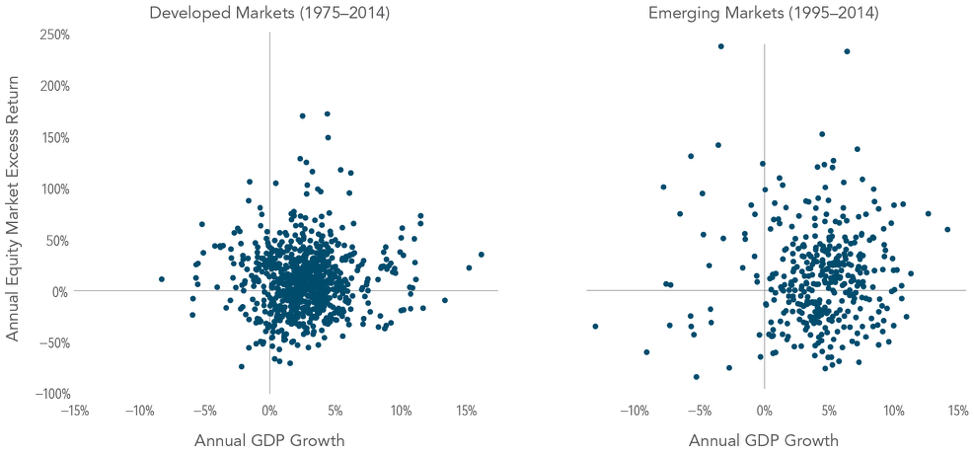

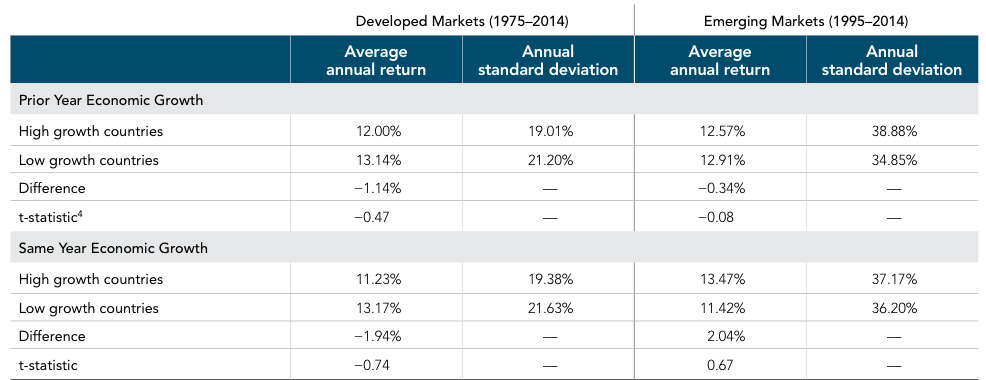

To be honest, I have my occasional conversational meanderings. My trouble is I can spend too much energy trying to convey a thought to someone with style and grace, that I sometimes miss the opportunity to be direct, succinct, on-point, and absolute. Below is a case in point. Over this past summer, I was gently scolded (in a fatherly way) by a long-time client who is an octogenarian. We were revisiting what would happen when he passed away. He wanted to know how his wife would continue receiving their income stream and other retirement benefits they had accumulated. During the course of this conversation, I kept referring to his death as his “passing away.” After a while, he finally had enough of me saying “passing away” and said Matt, “I’m going to DIE, but hopefully not today or tomorrow.” He asked me, “and where am I passing to or passing by; the bus station, the airport on my way to check out?” He said, with a quiet confidence, “I know where I’m going at my death.” He said, “I will die and you can refer to my passing as my death, there’s no need to be gingerly about it.” His point was well taken, it was unnecessary to be so sensitive to the issue as if he hadn’t thought about his own mortality. His point too was that it was almost impolite to be so delicate with a known fact—we’ve had a long established relationship. Ultimately, what he was trying to communicate to me was that we didn’t reconcile time in the same way, not because of our age difference but because if I didn’t come to the end of my meeting soon, he was going to die of hunger. Be direct, succinct and on-point, you’ll help your relationships live longer. Peace & Prosperity, Matthew D. Peck A relevant question for many investors is whether their view of economic growth should impact how they invest. Opinions about future economic growth often differ across market participants. For example, in a survey of more than 60 economists conducted by the Wall Street Journal in June 2016, estimates of US GDP growth in 2017 ranged from 0.2% to 3.7%.[1] A relevant question for many investors is whether their view of economic growth should impact how they invest. In this regard, they may be surprised to find that the historical link between annual GDP growth and equity returns has been quite weak. Exhibit 1 shows annual GDP growth vs. annual returns for developed and emerging markets. These plots indicate that there has not been a strong relation between GDP growth and equity returns in the same year. For example, in developed markets country/year combinations [2] when GDP growth was positive, the spread in returns was substantial: 323 country/year combinations had returns above 10% while 192 country/year combinations had returns below −10%. We see a similar pattern in realized returns for developed markets country/year combinations when GDP growth was negative. Emerging markets show a similar pattern. Exhibit 1. Annual GDP Growth and Equity Market Excess Returns  Sources: World Bank, MSCI, Morningstar. Shorter time periods shown for some countries due to data availability. Past performance is no guarantee of future results. See Data Appendix for details. Despite this weak relation between GDP growth and stock returns in the historical data, investors often ask whether shorter-term fluctuations in economic cycles impact stock returns in the near term. Stated differently, while on the surface Exhibit 1 presents a weak picture of GDP growth and stock returns in the same year, is there a relationship between the two that is not obvious from this exhibit? To address this question, we examine 23 developed markets from 1975 to 2014 and 19 emerging markets from 1995 to 2014.[3] Each year, countries are classified as either high or low growth depending on whether their GDP growth was above or below that year’s median GDP growth, defined separately for developed and emerging markets. We then look at stock market returns of high and low growth countries over the following year. The return for each group of countries is the average stock market return of all countries in the group weighted by countries’ market capitalization weights. Exhibit 2 shows that, historically, differences in GDP growth over the past year contained little information about differences in equity returns this year. In both developed and emerging markets, average annual returns were similar for high and low growth countries. In fact, low growth countries had slightly higher average returns than high growth countries, although this return difference was not reliably different from zero. In other words, there is no evidence that this return difference occurred by anything other than random chance. Exhibit 1. Equity Returns and Economic Growth in High and Low Growth Countries  Sources: World Bank, MSCI, International Finance Corporation (World Bank). Past performance is no guarantee of future results. Filters were applied to data retroactively and with the benefit of hindsight. Returns are not representative of indices or actual strategies and do not reflect costs and fees associated with an actual investment. Actual returns may be lower. Please see Data Appendix for more information. Can superior forecasts of short-term future economic growth help improve investment decisions? To address this question, we extend the analysis and assume perfect foresight about GDP growth over the next year. We now study the returns of high and low growth countries over the same year we measure GDP growth. This is not an implementable strategy because investors do not have the advantage of knowing economic growth in advance. They must rely on GDP forecasts, adding additional uncertainty. Exhibit 2 shows that even under the assumption of perfect foresight, using GDP data would not have generated reliable excess returns for investors. In developed markets, low growth countries had higher average annual returns than high growth countries, whereas in emerging markets, high growth countries had higher average annual returns than low growth countries. Neither difference in returns was reliably different from zero. This suggests that markets quickly incorporate expectations about future economic growth, making it difficult for investors to benefit from growth forecasts even with the advantage of perfect foresight. Differences in equity returns across countries seem to be driven more by differences in discount rates than by differences in GDP growth, even under a perfect forecasting scenario. Conclusion Many investors look to economic growth as an indicator of future equity returns. However, the relation between economic growth and returns in the historical data has been shown to be weak. This should not come as a surprise given that returns are determined by discount rates and investors’ aggregate expectations of future growth. Surprises relative to those expectations, whether positive or negative, may cause realized returns to differ from expectations. The evidence presented here suggests that differences in GDP growth contain little information about differences in stock returns in the same year and over the subsequent year. This means that it is difficult for investors to earn excess returns by relying on estimates of current or future GDP growth—even estimates that perfectly forecast GDP growth over the next 12 months. [1]. “Economic Forecasting Survey,” Wall Street Journal, http://projects.wsj.com/econforecast. [2]. Each observation in Exhibit 1 represents, for one country in one calendar year, the equity market excess return over one-month US Treasury bills as well as the rate of GDP growth. For example, one of the observations shows that in the US in 2014, the equity market excess return was 12.7% and GDP growth was 2.4%. [3]. See Data Appendix for details. 2015 GDP growth data was not available for most countries at the time of writing. [4]. A t-statistic is a measure for the reliability of an average return difference. Normally, a t-statistic of at least 2 in absolute value is necessary to reliably say that the result is different from zero. Data Appendix

Developed markets since 1975 (unless stated differently): MSCI Australia Index (net div.), MSCI Austria Index (net div.) (from 1980), MSCI Belgium Index (net div.), MSCI Canada Index (net div.), MSCI Denmark Index (net div.) (1980), MSCI Finland Index (net div.) (1988), MSCI France Index (net div.), MSCI Germany Index (net div.), MSCI Hong Kong Index (net div.), MSCI Ireland Index (net div.) (1988), MSCI Israel Index (net div.) (1999), MSCI Italy Index (net div.), MSCI Japan Index (net div.), MSCI Netherlands Index (net div.), MSCI New Zealand Index (net div.) (1988), MSCI Norway Index (net div.), MSCI Portugal Index (net div.) (1990), MSCI Singapore Index (net div.), MSCI Spain Index (net div.), MSCI Sweden Index (net div.), MSCI Switzerland Index (net div.) (1981), MSCI United Kingdom Index (net div.), and the MSCI USA Index (net div.). All of the following emerging markets are included since 1995 for Exhibit 1. For Exhibit 2, since 1995 (unless stated differently): MSCI Brazil Index (gross div.), MSCI Chile Index (gross div.), MSCI China Index (gross div.) (from 1996), MSCI Colombia Index (gross div.), MSCI Egypt Index (gross div.) (1998), MSCI Greece Index (gross div.), MSCI Hungary Index (gross div.), MSCI India Index (gross div.), MSCI Indonesia Index (gross div.), MSCI Korea Index (gross div.), MSCI Malaysia Index (gross div.), MSCI Mexico Index (gross div.), MSCI Peru Index (gross div.), MSCI Philippines Index (gross div.), MSCI Poland Index (gross div.), MSCI Russia Index (gross div.) (1998), MSCI South Africa Index (gross div.) (1996), MSCI Thailand Index (gross div.), MSCI Turkey Index (gross div.). A country is included in the analysis for Exhibit 1 in a given year if MSCI index return and GDP growth data are available and in the analysis for Exhibit 2 if MSCI index return, country weight, and GDP growth data are available. Returns are in USD. GDP growth is real GDP growth in local currency, converted to USD using constant 2005 USD as provided by the World Bank. Source: Dimensional Fund Advisors LP. All expressions of opinion are subject to change. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Past performance is no guarantee of future results. There is no guarantee an investing strategy will be successful. Cheers! Welcome to 2016! Winter is Coming! Oh wait, it is here in full swing in West Texas. I can’t help but to begin this Annual Review by mentioning the Great Texas Blizzard of December 2015. This winter weather system was an incredible act of nature. We would have to go back to the mid- 50s to recall such a historic snowfall and technical definition of “blizzard” conditions. All across the Texas South Plains snow estimates ranged from 2 to 20 inches of snow, with snowdrifts ranging from 3 ft. to 15 ft. in many places. As anticipated, many members of the community came together to volunteer their equipment and provide assistance to help dig out the surrounding communities. It was much appreciated! To some across the country it may seem that “Winter Storm Goliath” was no big deal. I offer this snowfall graphic for perspective. It was a massive snowstorm— if you live here you already knew that!

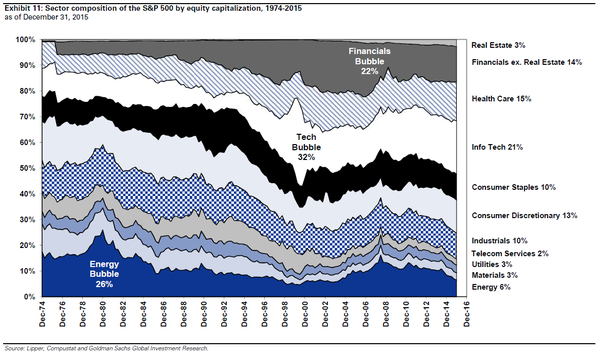

I also offer a link to a blog post called ‘Blizzards and Bullsh*t’ by blogger Dairy Carrie—I won’t apologize for the language, most of us read far worse on social media platforms. Her blog post provides in graphic detail the devastation cattle ranchers are currently facing and how challenging life can be for both dairy farmers and cattle ranchers. She also addresses a few asinine concerns animal activists have about why cattle are not all raised in barns. It’s an interesting and colorful post. Recent estimates indicate 30,000 head of cattle have been lost due to the winter storm. Blog link: http://dairycarrie.com/2015/12/30/winter-storm-goliath/#comments Winter Wonderland in Texas As for my family and I, we were glad to be able to enjoy the snowfall. Here’s a few pictures that captured our winter wonderland experiences in Texas.  My daughter standing in the middle of Hickory Street in Levelland, TX.  We captured this picture of a guy sledding on a car hood on Hickory St.  Not Lake Tahoe, Aspen or Telluride…Ski Apache, NM, an 85” snow base. Best snow I’ve ever experienced at Ski Apache! Update On Oil Prices—Who Knows? A noted junk bond manager recently quipped that “there’s nothing intelligent to say about the future price of oil.” There’s much more to this context but I mostly agree. I’m eating my words from this time last year when I mentioned that the oil price decline would be a powerful shot in the arm for global growth—my goodness. I will avoid a folly opinion and point to a graphic highlighting what I hope is more interesting and important to disciplined investors.  Asset bubbles real or perceived should not be a reason for avoiding the stock market altogether. As one market segment tanks, others will do well. For long-term, highly diversified, disciplined investors, “bubbles” don’t matter. The danger occurs when you concentrate risk and put too much emphasis on a particular asset class or market sector. You will never know when a “bubble” will burst. If you recall the recent Oil Bubble Bust came early last fall with no warning, for no particular rhyme or reason. This is of course coming from an investment standpoint. If you are employed by the oil industry, your focus is maintaining employment, and I empathize. Venerable or Vulnerable Vanguard, Accusations of a Tax Evasion Scheme I first read about this whistleblower lawsuit against Vanguard in August of 2014, I found it very curious and eagerly waited for more details. Surprisingly, this story has not caught the attention of others in the very opinionated advisory community. Personally, I find these allegations against Vanguard the most interesting topic of personal finance in all of 2015. I would not describe myself as a “boglehead,”—a term that is used to describe a devotee to Vanguard’s approach to investing based on the name of John Bogle, the founder of Vanguard. Though, I do have a healthy respect for the world’s largest mutual fund company. In fact, within the firm we do often recommend Vanguard funds and our family owns a couple Vanguard funds. Essentially, about 2 years ago, David Danon, a former Vanguard tax attorney (the whistleblower) filed formal complaints with the Internal Revenue Service and other state taxing agencies claiming that Vanguard’s low fees are an illegal tax scheme. He lays out an argument that Vanguard should have charged investors almost $20 billion in investment management fees and claims that Vanguard owes around $35 billion in taxes, interest and penalties going back to 2007. In the details of his whistleblower allegations, he cites IRS Code Section 482 that requires transactions between related companies to take place at the same price as if the companies were unrelated. Mr. Danon believes that Vanguard provides services to its mutual funds/related entities at “artificially low, at-cost” prices, skirting accepted U.S. tax law. Because of its unique business structure, Vanguard shows little to no profit despite managing nearly $3 trillion in assets. Mr. Danon asserts that Vanguard’s business structure enables the company to underprice competitors to gain an unfair advantage and its dominance in the industry is related to tax evasion. These allegations are incredible to say the least! There does seem to be a bit of merit to the case and the allegations, as other states have been reviewing Vanguard’s financial reporting. Texas was the first state to reach a settlement with Vanguard over back taxes. It marks the first payout from Mr. Danon’s contention that Vanguard has not been forthcoming with its accounting between entities—though Vanguard claims the settlement is from a routine tax audit. In news reports it does appear that Mr. Danon was able to receive whistleblower compensation for the Texas settlement. So what does this ultimately mean for Vanguard mutual fund investors? It’s still too early to know for sure, there are many complexities. If the IRS decides to get involved and settlements are reached, mutual fund expense ratios could go nominally higher, as hefty amounts of taxes could be owed. Vanguard is an enviable and mighty competitor in the investment management industry. In 2015, it raked in $76 billion in new cash from investors. The company has a large mark on its back and I anticipate taxing authorities and competitors will all want a piece of Vanguard’s perceived troubles. Link to a white paper abstract from Reuven S. Avi-Yonah, University of Michigan Law School – Too Big to Tax? Vanguard and the Arm’s Length Standard http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2666426 A New Year Brings New Speculation In this last section, I will repost the thoughts of Jim Parker of Dimensional Fund Advisors. As you will read, Jim highlights the folly of financial predictions. We all have thoughts and opinions about what could be. Jim lists 10 predictions you can count on coming true in 2016. 2016: Ten Predictions to Count OnBy Jim Parker, of Dimensional Fund Advisors

The New Year is a customary time to speculate. In a digital age, when past forecasts are available online, market and media professionals find it harder to hide their blushes when their financial predictions go awry. But there are ways around that. The ignominy that goes with making bold forecasts was highlighted in a recent newspaper article, which listed many bad calls US economists had made about 2015. These included getting the timing of the Federal Reserve’s interest rate increase wrong, incorrectly calling for a rise in long-term bond yields, and assuming an end to the commodity rout.1 For the broad US equity market, 22 strategists polled by the Wall Street Journal2 estimated an average increase for the S&P 500 of 8.2% for 2015. The most optimistic individual forecast was for a rise of 14%. The least optimistic was 2%. No one picked a fall. As it turned out, the benchmark ended marginally lower for the year. In the UK, a poll of 49 fund managers, traders, and strategists published in early January 2015 forecast that the FTSE 100 index would be at 6,800 by midyear and 7,000 points by year-end. As it turned out, the FTSE surpassed that year-end target by late April to hit a record high of 7,103 before retracing to 6,242 by year-end.3 Australian economists were little better. The consensus view, according to a January 2015 Fairfax Media poll, was that local official interest rates would stay on hold all year. The Reserve Bank of Australia proved that wrong a month later, before cutting rates again in May. It shouldn’t be a surprise that if economists can’t get the broad variables right, it must be tough for stock analysts to pick winners. Even a stock like Apple, which for so many years surprised on the upside, disappointed some forecasters last year with a 4.6% decline.4 In Australia, the “Top Picks for 2015” published by one media outlet a year ago included such names as Woodside Petroleum, BHP Billiton, Origin Energy, and Slater & Gordon, all of which suffered double-digit losses in the past year.5 It should be evident by now that setting your investment course based on someone’s stock picks or expectations for interest rates, the economy, or currencies is not a viable way of building wealth in the long term. Markets have a way of confounding your expectations. So a better option is to stay broadly diversified and, with the help of an advisor, set an asset allocation that matches your own risk appetite, goals, and circumstances. Of course, this approach doesn’t stop you or anyone else from having or expressing an opinion about the future. We are all free to speculate about what might happen in the economy and markets. The danger comes when you base your investment strategy on such opinions. In the meantime, if you insist on following forecasts, here is a list of 10 predictions you can count on coming true in 2016:

You can see from that list that if forecasts are so hard to get right, you are better off keeping them as generic as possible. Like a weather forecaster predicting wind, hail, heat, and cold over a single day, your audience should prepare themselves for all climates. The future is always uncertain. There are always unexpected events. Some will turn out worse than you expect; others will turn out better. The only sustainable approach to that uncertainty is to focus on what you can control. In the meantime, let me wish a happy new year to you all. 1. Malcolm Maiden, “The Year Market Economists Failed to See Coming,” SMH, December 30, 2015. 2. “Strategists Expect Stocks to Keep Climbing in 2015,” Wall Street Journal, January 2, 2015. 3. “Five Fund Strategies to Ride Rising Markets,” The Times, January 3, 2015. 4. “Seven Stocks to Buy for 2015,” CNN Money, December 31, 2014. 5. “Top Stock Picks for 2015,” Motley Fool. I look forward to visiting with you in 2016. Be ready to hang on to your hat, 2016 is already interesting. Regards, Matthew D. Peck Client Advisor & Partner Amicus Financial Advisors, LLC Dear Clients and Friends,

As of this writing we duly note the following:

Happy New Year! What a stressful but productive year for the economy and U.S. stock market. There are no shortages of headline events that would “normally” rattle the markets. This is U.S. resiliency at its best. To describe the year 2014 with a pun, my literary description would be that the U.S. economy is acting like—a rebel with a cause, when compared to the rest of the world. The U.S. economy is in recovery mode with quarterly GDP estimates continually being revised upward. While this is a lagging economic indicator, these are steps in the right direction. Other areas signaling positive economic growth are car and truck sales, and for what it’s worth the end of Federal Reserve stimulus via quantitative easing. To move forward in 2015 and beyond, middle-class wage growth and a more confident global consumer will be required to fuel economic growth and to support higher asset prices. Oil Patch Pain The precipitous decline in the price of oil was largely unforeseen and I don’t see any “experts” that will be able to successfully call the bottom in this troubling commodity price decline. What I do see is an instant increase of disposable income for consumers. Oil price declines are providing relief at the pump and a jingle in the pocket of consumers. If the price of oil stabilizes in the coming months, it would provide a powerful “shot in the arm” to global growth—a viewpoint that is currently being underestimated. Lower oil prices would provide a market-based, natural economic stimulus rather than the faux-stimulus that the global central banks provide in the form of interest rate cuts in an already low-interest rate environment. Wide Dispersion of Returns—U.S. Large Cap vs. Global Equities In reviewing asset class performance, it’s painfully noticeable that global equities (particularly emerging markets) have substantially underperformed the U.S. markets for years now. I offer this empathetic reminder that your portfolio is properly diversified when there’s a portion of it that causes grief or frustration. Rather than focus on the grief in your portfolio, recognize that periods of over- and underperformance are normal when investing in a globally diversified portfolio. Performance will shift when you least expect it. Using the MSCI EAFE Index as a historical gauge, these periods of underperformance last about 5 years—going back to 1970, when the index was introduced. The idea is to have time in an asset class and not to market time (trade frequently) an asset class. We are long-term investors in global stocks. Benchmark Indexes 5-Year, Average Returns through 2014 S&P 500 Index 14.59 MSCI EAFE 4.29 MSCI World Ex-US 4.16 MSCI Emerging Mkt USD -1.51 Source: Morningstar FOMO Risk—Fear of Missing Out A respected investment manager that I follow, Howard Marks of Oaktree Capital Management, describes FOMO risk as “the risk that comes from the excessive fear of missing out” on investment opportunities. This fear is a risk factor because it leads investors to do the following: to take more risk than necessary, to invest in securities they don’t understand, and to chase investment returns (to buy high, rather than to buy low) at inopportune times. I caution folks to be mindful of this as U.S. markets reach multi-year highs. Don’t invest because you feel like you have missed out, invest because there is an ultimate goal to achieve further down the road. We look forward to visiting with you in 2015. Thank you for your trust and confidence. Peace and Prosperity, Matthew D. Peck Client Advisor & Co-Managing Member Amicus Financial Advisors, LLC  Many of my posts pertain to the markets and the economy. I have my rants and raves about this or that; from the direction of interest rates and federal reserve policy, to stock market volatility—all the fun, opinionated aspects of having a blog. This post, I’d like to highlight our use of technology and provide a few technology-driven solutions to client-specific needs. Within the firm, our service offering continues to evolve. The needs of our clients drive our desire for continuous improvement. The efficiencies that technology delivers, gives us a unique competitive advantage and allows our firm to provide services at a reasonable cost across multiple brokerage and custodial platforms. Let me provide a couple of examples. Client Need 1: I need help managing my retirement accounts provided through my employer? Clients understand that our primary custodians for housing and managing client assets are Schwab and Fidelity—it’s where their assets are held. We provide investment advisory services to their brokerage accounts, IRAs, and certain types of trust accounts. Typically, we would only provide our reporting services to the accounts we managed, leaving most qualified plan accounts such as a 401k, 403b, 457, variable annuities and restricted stock awards left out of the fold from an advisory standpoint. Times have indeed changed and technology allows our firm to aggregate, manage and provide comprehensive advisory reporting on client assets that are “held away” at other firms. This means those accounts that are not-managed, (what we call “self-directed”) or not part of a complete investment strategy, can be brought in to our advisory services platform and included in our comprehensive advisory relationship. How it works. With the appropriate client permissions in place, our service provider gathers the login credentials for each client account that is “held away.” Then our portfolio management system securely and safely gathers account data for importation. Once “held away” accounts are in our system we can begin the process of building a complete portfolio that is appropriate for clients individual preferences, risk tolerance and time horizon. Adjustments to a client’s Investment Policy Statement (the “blue print” and process for how assets are managed) will then be updated and maintained. We take on the responsibility of monitoring investment managers, changes to the investment lineup, trading and rebalancing of the account—the same duties and tasks we would customarily provide. What is the advantage? It’s no secret that employees that participate in employer-provided retirement plans have little or no access to specific and individually tailored investment and retirement planning advice. Employers and plan providers do their best to provide a minimal amount of information but the end result is employees making a minimum informed decision about their retirement accounts. Now, our client relationships will have the confidence that all of their brokerage and retirement accounts can be managed for optimum results. It provides a confidence to clients knowing that all investment assets are being managed consistently, cost-effectively and thoughtfully—no matter where the assets are held.  Client Need 2: Account Aggregation and Performance Reporting for Multiple Advisors/Managers

There are many relationships where our firm is one of several investment advisors/managers in a client’s overall portfolio. A client in this situation could be a foundation, a trust, a qualified plan or simply a high-net worth individual. Each particular investment manager plays a specific role in the portfolio. They may manage the fixed income portion or represent the passive (index fund) investments of a portfolio. There are several administrative challenges that these types of clients face. One of the greatest challenges is aggregating the individual accounts/managers into one consolidated set of reports for review and management. Traditionally, one advisor is selected for this task and the role is fraught with expense, a lack of timeliness and (in general) inaccuracies in reporting. Ideally, this is a level of reporting that would provide a greater degree of transparency, proper performance measurement and portfolio detail far better than the usual quarterly brokerage statement. While this service offering is not new, it’s traditionally reserved for institutional-based clients. Comprehensive Advisory Reporting The solutions we that can provide is an accurate and thorough reporting for all managers at an individual and at a consolidated view with daily reconciliation. Also, we provide a web portal that a client can conveniently access. This means that critical portfolio data can be immediately accessible to the decision-makers: the investment committee, a board at-large or the hands-on, individual high-net worth investor. Depending on the level of service a client desires; we can act as an investment fiduciary and provide an advisory role, or simply provide a comprehensive reporting role and report on an as-needed basis. Client demand has prompted our firm to offer a more complete service offering. It has always been a goal of mine to maintain a close-knit, boutique-style advisory firm with all the institutional capabilities of a much larger firm. I like to think of our capabilities as “quarterbacking” for the team. A leadership role where we help clients maintain existing advisory relationships, build new relationships with our firm and work together as a team. My friends thank you for your ongoing support, trust, confidence and feedback. Peace and prosperity, Matthew D. Peck Client Advisor & Partner Amicus Financial Advisors, LLC |

Archives

March 2021

Categories |

RSS Feed

RSS Feed